Launched in 27 Cities Worldwide

Jessica | Upstream

Intelligent Cars Reference | WeChat Official Account AI4Auto

China’s Robotaxi sector has once again broken through the ceiling of what this business can do.

Baidu has released its earnings report, along with the latest data for Apollo Go. Robotaxi weekly order volume has peaked at over 350,000, while the daily average ceiling has reached 50,000.

Over the past two months, Apollo Go’s cumulative ride count increased by 2 million, and its cumulative fully driverless mileage rose by 30 million kilometers.

Apollo Go can now be seen in 27 cities around the world. In some major domestic cities, it has already reached break-even on a per-vehicle basis.

As fleet size grows and operating areas continue to expand, it may not be long before driverless cars are arriving right at your doorstep.

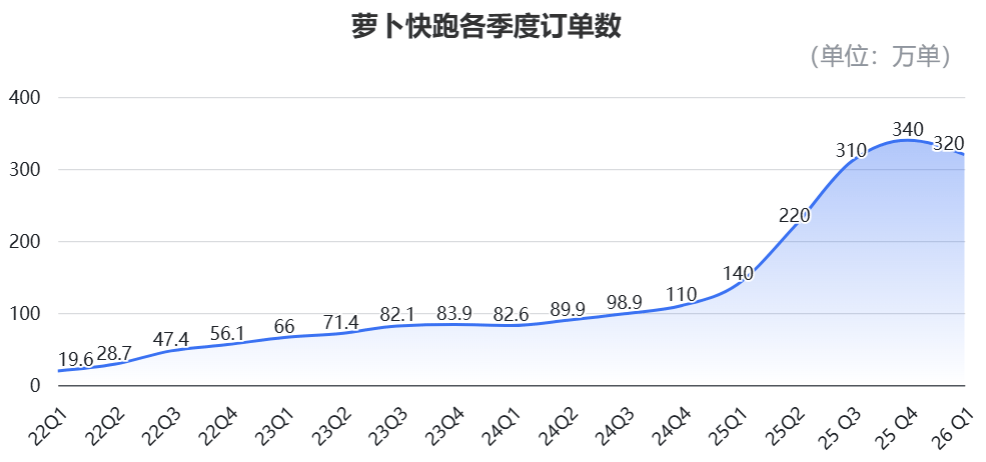

In the first quarter of this year, Apollo Go provided 3.2 million fully driverless mobility services, up about 129% year over year.

At the same time, Baidu disclosed that Apollo Go’s weekly order peak had already exceeded 350,000 as of March.

To put that in perspective, at peak levels, Apollo can handle up to 50,000 Robotaxi services per day — or roughly 34 orders per minute.

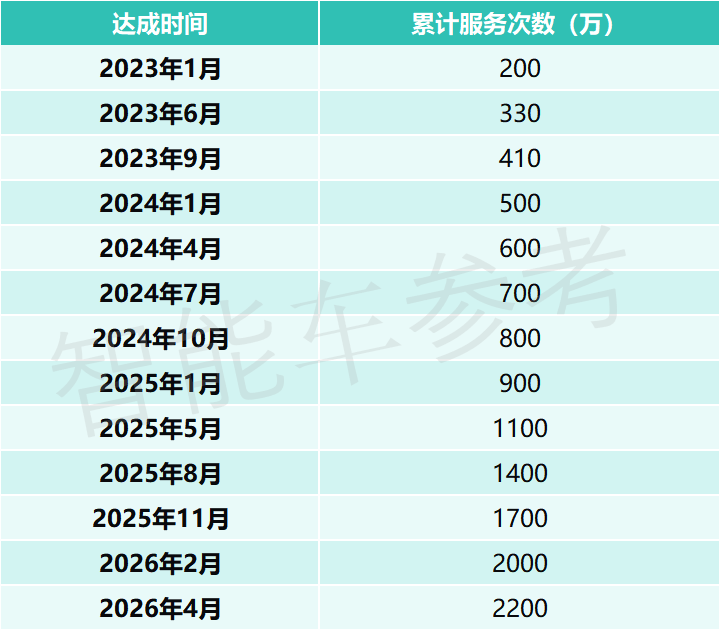

As of April this year, Apollo Go’s cumulative orders for consumer-facing autonomous mobility services had already exceeded 22 million.

Its total autonomous driving mileage has surpassed 330 million kilometers, of which 220 million kilometers were fully driverless.

Compared with the latest data released in the previous quarter’s earnings announcement in February, Apollo Go added 2 million cumulative rides over the past two months, and its cumulative fully driverless mileage increased by 30 million kilometers.

Roughly speaking, that means the average distance per Robotaxi order over the past two months was 15 kilometers.

For everyday travel, 15 kilometers falls into the medium to short-medium range, which also suggests that Apollo Go’s services are in practice more focused on commuting, cross-area trips, and airport or railway station transfers.

Looking at its operating footprint, Apollo Go has already expanded to 27 cities worldwide.

Domestic operating cities include Wuhan, Beijing, Shanghai, Guangzhou, Shenzhen, and the Chengdu-Chongqing region, and it also covers parts of Hong Kong.

Overseas, it has expanded into Abu Dhabi and Dubai in the Middle East, as well as Seoul in South Korea, and has recently begun road testing in Switzerland.

Its expansion in the Middle East has been especially notable. The app launched in Dubai in March has now been officially released, making Apollo the first, and currently only, autonomous mobility platform in the region with a dedicated standalone mobility app.

In addition, according to Robin Li, the first batch of driverless vehicles for London has already arrived, and Apollo Go will soon begin testing there alongside Uber and Lyft.

Meanwhile, Waymo, another top-tier Robotaxi player across the Atlantic, also revealed its latest progress in the recent earnings report of Google’s parent company.

Waymo’s driverless vehicles are operating in 11 cities worldwide, and its fully autonomous mobility services have surpassed 500,000 rides per week.

That said, neither company has disclosed its latest fleet size. From the outside, all that can be seen is steadily rising order volume and ever-expanding city coverage.

Still, the more there is to do, the less is said — which is itself a sign that the industry has already entered a new stage of competition.

Robin Li: In Some Major Domestic Cities, We’ve Already Turned Profitable

As leading players race to commercialize faster, “monetization” has become an increasingly watched topic from the outside. But that is not Apollo Go’s top priority at the moment.

According to Robin Li, the localized operating data Apollo Go has accumulated in the domestic market has already enabled the formation of highly mature autonomous driving algorithms and an operating system.

On that basis, Apollo Go has achieved break-even on a per-vehicle basis in its largest domestic operating city, and it has done so while maintaining relatively low pricing.

What’s more, this model is replicable and can support broader market expansion. For example, Apollo Go’s move from Hong Kong to London into right-hand-drive markets is grounded in its accumulated operating experience.

At the same time, overseas markets generally offer more room on pricing and are easier to turn profitable. The company expects overseas profitability to potentially exceed that of the domestic market as the business scales.

That said, Robin Li also noted that the autonomous mobility industry is still in its early stages, and the business model has in fact not yet been fully defined.

For that reason, Apollo Go’s strategic focus at this stage remains on expanding operating scale, deepening core technologies, and strengthening operational advantages.

In addition to standard Robotaxi services, Apollo Go is also exploring new implementation scenarios to broaden the path to commercial monetization for driverless vehicles.

According to Robin Li, Apollo Go has partnered with CAR Inc. to jointly launch an autonomous vehicle rental service. Driverless cars have been directly deployed at the arrival level of Haikou Airport in Hainan Province, where passengers can access them immediately.

Robin Li said that Apollo Go is now in a phase of scaling up the business, and that the core of its development is to deeply integrate autonomous mobility services into the city’s public transportation system, its day-to-day urban operations, and people’s everyday lives.

What Did Baidu’s First-Quarter Results Look Like?

When people think of Baidu, the first thing that usually comes to mind is still its search engine.

But looking at its announced Q1 2026 earnings, this company has quietly been undergoing a major shift.

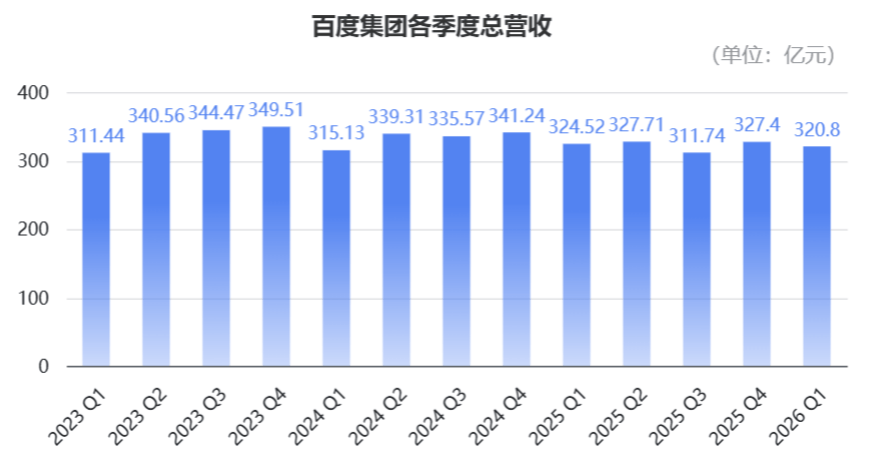

Let’s start with the big picture. Baidu reported total revenue of RMB 32.1 billion in the first quarter of this year, down 2% from the previous quarter, but overall remaining stable.

Among that, revenue from online marketing services, long one of its main income sources, came in at RMB 12.6 billion this quarter, down 22% year over year and 17% quarter over quarter. Its share of total revenue from Baidu’s core business also fell from 63% in the same period last year to 48%.

By contrast, other revenue driven mainly by smart cloud and AI services reached RMB 13.4 billion this quarter, up 42% year over year and 23% quarter over quarter. Its share rose from 37% to 52%, surpassing online marketing services for the first time.

At the center of this structural shift is what Baidu defines as its “core AI new businesses.”

Revenue from AI-related new businesses in Baidu’s core operations reached RMB 13.6 billion, up 49% year over year. More importantly, it accounted for more than half — 52% — of Baidu’s core business revenue for the first time.

In other words, AI has already become a real pillar of Baidu’s revenue.

Baidu CFO He Haijian said in the earnings call that total revenue from Baidu’s core businesses increased 2% year over year, returning to positive growth. Non-GAAP operating profit from core businesses rose 39% quarter over quarter to RMB 4 billion, while operating cash flow remained positive at RMB 2.7 billion.

These figures indicate improving operational efficiency and stronger overall business health at Baidu.

Looking at the breakdown, the most prominent part of Baidu’s AI new businesses is undoubtedly its smart cloud infrastructure.

Revenue in this area reached RMB 8.8 billion in the first quarter, up a substantial 79% year over year. Among them, GPU cloud revenue grew even faster, surging 184%.

This reflects the rapid release of enterprise demand for AI computing power, and shows that Baidu’s infrastructure-layer investments are starting to pay off.

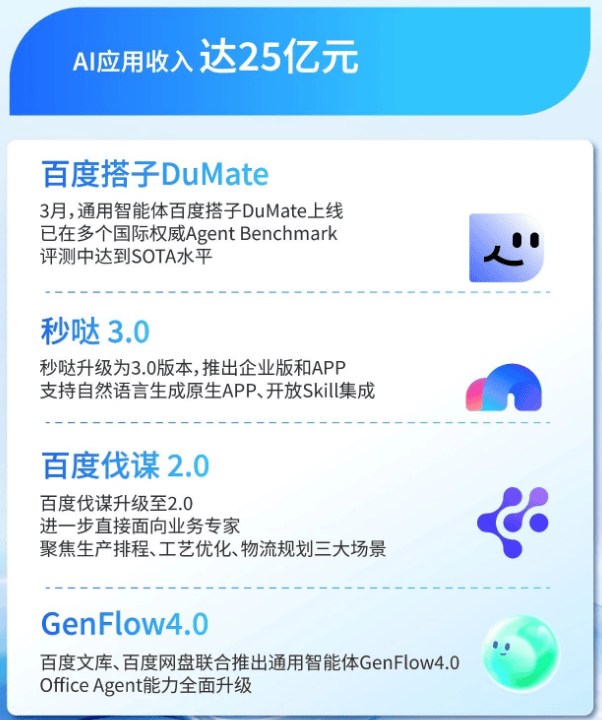

By contrast, AI application revenue was RMB 2.5 billion, basically flat year over year. While the growth rate is less eye-catching than cloud, Baidu is still making steady progress at the application layer.

For example, DuMate, a general-purpose agent launched in March this year, can automatically handle complex tasks such as cross-app operations and file manipulation. Baidu also has its no-code development platform “Miao 3.0” and its self-evolving Agent2.0, the latter of which set a new industry benchmark in machine learning engineering tests.

Although these products are still in the early stages, they are already contributing to Baidu’s technical reputation and user base expansion.

On the marketing side, Baidu is also using AI capabilities to reshape its revenue structure.

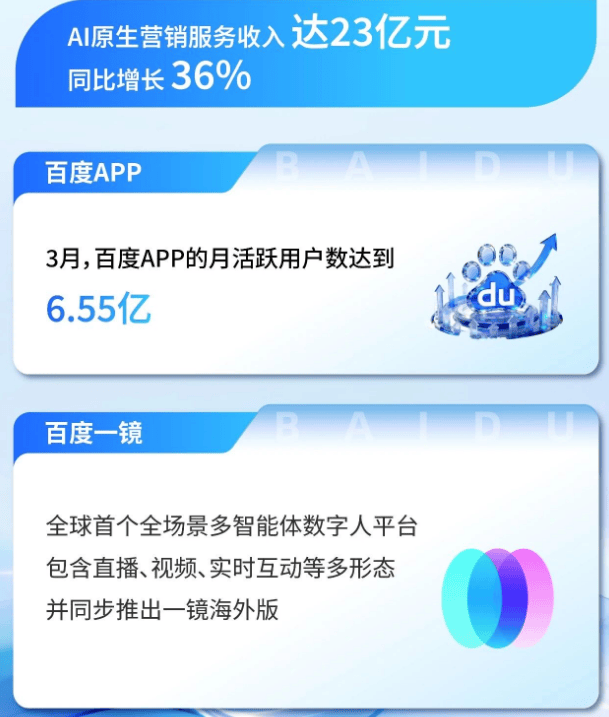

In the first quarter of this year, the company’s AI-native marketing services generated RMB 2.3 billion in revenue, up 36% year over year.

Although Baidu’s overall online marketing services revenue fell 22%, the growth in AI marketing is gradually offsetting the decline in traditional advertising. Baidu App’s monthly active users also remained stable at 655 million, preserving its massive user base.

On the profitability front, Baidu’s operating profit for the first quarter was RMB 3.2 billion, with an operating margin of 10%.

Net profit for the period was RMB 3.4 billion, and non-GAAP net profit was RMB 4.3 billion. While both were down from the same period last year, overall they remain at healthy levels.

Taken together, the first quarter of this year already showed a shift in the engine driving Baidu’s revenue growth: traditional businesses are adjusting steadily, while the new AI businesses are rapidly taking over the baton.

Baidu is quietly entering a new growth cycle. The Baidu you know is no longer just a search company.